Community Health Systems, Inc.

’s

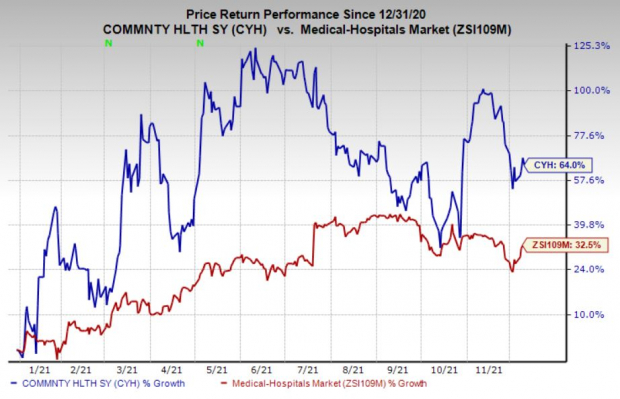

CYH

shares have jumped 64% in the year-to-date period, outperforming the 32.5% growth of the

industry

, thanks to the growing demand for healthcare services. The company has not only managed to navigate through last year’s coronavirus-induced market volatility but also positioned itself for better returns in the future.

Image Source: Zacks Investment Research

The hospital industry suffered in 2020 due to the postponement of elective surgeries amid the pandemic. It has regained momentum this year on the back of recovering volumes. Headquartered in Franklin, TN, Community Health benefited from the recovery in volumes. It is a leading operator of general acute care hospitals and outpatient facilities in communities across the United States. It currently has a market cap of $1.6 billion.

Can It Retain Momentum?

The answer is yes and before we get into the details, let us show you how its estimates for 2021 stand. The Zacks Consensus Estimate for 2021 earnings per share stands at $1.67, signaling a significant increase from last year’s figure of 45 cents. The consensus estimate for 2021 revenues is pegged at $12.3 billion, indicating a rise of 4.1% from 2020.

The company beat earnings estimates in all the last four quarters, with an average of 675%.

Now let’s delve into what’s driving the Zacks Rank #3 (Hold) stock.

Business Expansion

: The company is focused on increasing facilities. In the 2018-2020 period, it added 250 beds along with 50 new surgical and procedural suites. In 2020, CYH launched a micro hospital in Tucson and a replacement hospital in La Porte, IN. It also unveiled three new ambulatory surgery centers and freestanding emergency departments each. The company opened two new hospitals in Indiana and Arizona. It recently invested in bed and service line expansions in Birmingham, Naples, Huntsville and Knoxville, etc. CYH has a pipeline of activities lined up for the near future. Community Health’s Lutheran Downtown Hospital in Fort Wayne is expected to come online in the fourth quarter of 2021. The Tucson East De Novo Hospital is likely to commence operations in first-quarter 2022. Further, it has de nono and expansion projects for inpatient facility development as well as service line expansion projects for cardiac, neuroscience, and post acute & specialty in the growth pipeline. We expect the company to gain momentum from all these strategic initiatives.

Inorganic Growth

: CYH has been gaining from a series of acquisitions over the past several years. It generally targets the hospitals that cater to relatively non-urban and suburban communities wherein management can add value through specialty medical service expansion, economies of scale, additional investment in new technology and improved process management. CYH’s subsidiary, Northwest Healthcare, signed a joint venture with

Select Medical Holdings Corporation

SEM

to acquire Curahealth Tucson in June 2021.

Telehealth Services:

The company made investments in telehealth, which gained substantial response amid the COVID-19 environment. On an annualized basis, it managed to deliver around 650,000 telehealth visits. We expect the demand for telemedicine to continue, given its efficiency and popularity.

Upbeat Guidance:

Following third-quarter results, the company upwardly revised its 2021 guidance. Adjusted EBITDA is now anticipated within $1,780-$1,820 million, higher than the previous projection of $1,700-$1,800 million. Net operating revenues are now projected in the range of $12,150-$12,350 million versus the prior guidance of $11,900-$12,300 million. Capex is now expected in the range of $450-$500 million. A solid guidance should instill investors’ confidence in the stock.

Reducing Expenses

: The company’s restructuring initiatives lowered costs to a great extent. In 2018, 2019, and 2020, operating costs and expenses declined 12%, 19.1%, and 15.1% year over year, respectively. Operating costs as a percentage of net revenues declined to 90.4% as of Dec 31, 2020 from 95.1% at 2019-end. Although the same increased 2.2% in the first nine months of 2021, we expect the metric to decline going forward. The company is constantly monitoring operational activities to cut costs. Going forward, its expenses are expected to improve further on the back of a planned business rejig.

Risks

Despite the upside potential, there are a few factors that are impeding the stock’s growth lately. At third quarter-end, the company had only $1.3 billion in cash and cash equivalents. Its long-term debt was recorded at $11.9 billion as of Sep 30, 2021. Balance sheet weakness can affect the company’s financial flexibility. Also, a weak cash flow situation is concerning. For the nine months ended Sep 30, 2021, net cash provided by operating activities of $400 million plunged from the year-ago comparable figure of $2.1 billion. Nevertheless, we believe that a systematic and strategic plan of action will drive long-term growth.

Stocks to Consider

Some better-ranked players in the

Medical

space include

ADMA Biologics, Inc.

ADMA

and

Aptose Biosciences Inc.

APTO

, each having a Zacks Rank #2 (Buy). You can see

the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here

.

Based in Ramsey, NJ, ADMA Biologics is a leading biopharmaceutical company. ADMA is devoted to developing a pipeline of plasma-derived therapeutics. It creates and markets specialty plasma-derived biologics for immune deficiencies treatment. Also, ADMA Biologics operates various source plasma collection units. ADMA’s bottom line for 2021 is expected to jump 39.8% year over year. Its earnings estimates have witnessed two upward estimate revisions in the past 30 days compared to none in the opposite direction. ADMA Biologics beat earnings estimates twice, met once and missed on the other occasion in the last four quarters.

Aptose Biosciences — based in Toronto, Canada — develops personalized therapies for oncology-related needs in the United States. Its license agreement with Hanmi Pharmaceutical for Clinical Candidate HM43239 can be a major positive. APTO’s bottom line for 2021 is expected to jump 1.5% year over year. The company’s earnings estimates have witnessed two upward movements and no downward revision in the past 30 days. Aptose Biosciences beat earnings estimates twice in the last four quarters and missed the same on the other two occasions, delivering an earnings surprise of 7%.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2021. Previous recommendations have soared +143.0%, +175.9%, +498.3% and +673.0%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report