Mining stocks have come into focus of late because of the war in Ukraine and sanctions on Russia that are limiting the normal flow of minerals around the world. That’s particularly true because Russia is a big exporter.

But mining is generally not considered to be a high-growth sector. In fact, it is a major pollutant, which is why governments across the world are taking policy decisions to curtail output, or at least setting and implementing sustainability goals.

The main issue with mining is the amount of energy (mainly fossil fuels) it uses, which has a huge environmental impact. This is made worse by the fact that good deposits with significant ore availability are getting harder to find. When the ore is not available in sufficient quantities, miners require even more energy to extract it.

The growing costs of mining, when coupled with the high cost of equipment, often makes the extraction of such ores unviable. Only things like precious metals and rare earths may be worth extracting because they fetch a very high price and are therefore able to absorb higher costs.

Precious metals like gold, silver and platinum are often treated as a safe haven for investors in uncertain economic situations such as now. The Fed is focused on lowering inflation, which is being exacerbated by a number of factors including a still-hot housing market, supply chain disruptions, constraints in semiconductor supply, a very tight labor market and still-high amounts of cash that entered the economy via the Fed’s rescue plan for COVID 19.

This is being achieved through monetary policy, mainly interest rate increases. But there’s also the fear that a sharp response from the Fed could trigger a recession, and this is the main factor driving demand for precious metals right now. And as always, the increased demand from investors is pushing up prices.

As far as rare earths are concerned, they are essential for technological progress, including toward a greener future. Some of the latest technology uses these substances in significant quantities. But rare earths as the name indicates, are hard to extract because they occur in traces. Moreover, they aren’t available at all in many places. So there’s a global drive (led by China) to secure the sources of these materials.

As in the case of rare earths, it is the earth itself that has the answers to many of our problems. And so, although coal is considered one of the dirtiest fossil fuels because of its polluting characteristic, this resource is playing a big role today in dealing with the energy crisis that has resulted from the Russia-Ukraine conflict.

So although many coal companies have cut back operations, they are doing very well in the current environment. Particularly because oil companies are not going out of the way to increase the number of drills, which is keeping supply constrained and prices attractive for all energy suppliers.

It’s also important to remember that mined materials are essentially raw materials that are converted to finished products for consumption. A general expansion in manufacturing activity is a positive indicator of demand since it means that more materials are being used.

One economic indicator of expansion in manufacturing is the Purchase Managers Index (PMI). Whenever the PMI reads above 50, there is expansion in the manufacturing sector while a reading below 50 indicates contraction. In a recession, there is usually a contraction in manufacturing.

The PMI is available on a monthly basis. And over the past year, it has remained well above 50. Its dip in January to around 55 may have caused some concern, but the number has jumped back since then. In March it was 58.8. This is an indication that manufacturing demand remains strong.

The above factors indicate that this is a good time to be investing in mining stocks. The Zacks Industry Rank of 46 allotted to the Mining – Miscellaneous industry out of 250+ such industries also places the industry in the top 18% of Zacks classified industries.

Zacks research shows that industries placed in the top 50% are more likely to significantly outperform the bottom 50% and contribute to share price appreciation of constituent stocks. So I’ve listed a few worth considering right now:

Glencore plc

GLNCY

Baar, Switzerland-based Glencore refines, processes, stores, transports, and markets metals and minerals, and energy products in the Americas, Europe, Asia, Africa and Oceania. Its two operating segments are Marketing Activities and Industrial Activities. The company produces and markets copper, cobalt, nickel, zinc, lead, gold, silver, ferrochrome and other minerals. It also engages in the oil exploration/production, distribution, storage, and bunkering activities and produces thermal, metallurgical and semi-soft coal.

Glencore is seeing solid estimate revisions. In the last 60 days, its 2022 earnings estimate has gone from $1.59 to $2.62, an increase of around 65%. The 2023 estimate increased from $1.37 to $1.92, or 40%. Revenue and earnings are currently expected to grow 106% and 152% in 2022.

The Zacks Rank #1 stock has Value and Growth Scores of A.

Teck Resources

Ltd.

TECK

Vancouver, Canada-based Teck Resources Limited is a diversified company engaged in exploration; development; and processing, including smelting and refining of met coal, copper, zinc and energy products. The company’s principal products include steelmaking coal; copper concentrates and refined copper cathodes; refined zinc and zinc concentrates; energy products, such as bitumen; and lead concentrates. It also produces molybdenum, gold, silver, germanium, indium, mercury and cadmium, as well as chemicals, industrial products and fertilizers.

Teck Resources also holds interest in oil sands projects. As of Dec 31, 2021, it owned or had interests in 13 operating mines, a large metallurgical complex, and several major development projects in the Americas. The company expertise includes a wide array of activities related to.

Teck Resources missed last quarter’s earnings estimate by a sliver although sales missed by around 6%. But analysts are extremely optimistic about 2022 and beyond. So they’ve taken the 2022 estimate up $2.13 (41%) and the 2023 estimate up $2.00 (63%). This represents 32% revenue growth and 62% earnings growth this year.

Sibanye Gold Ltd.

SBSW

Sibanye Stillwater, the Johannesburg, South Africa-based precious metals mining company, has a diverse portfolio of platinum group metal and gold operations and projects. It produces gold; platinum group metals (PGMs), including palladium, platinum and rhodium; and by-products, such as iridium, ruthenium, nickel, copper and chrome.

Analysts have been raising estimates for Sibanye’s earnings. The 2022 earnings estimate is up 85 cents (24%) and the 2023 estimate is up 82 cents (29%) in the last 60 days. At the current level, the estimates reflect 2022 revenue and earnings growth of 40% and 32%, respectively.

The Zacks Rank #1 stocks has a Value Score of A and Growth Score of B.

Alpha Metallurgical Resources, Inc.

AMR

Bristol, Tennessee-based Alpha Metallurgical Resources is a mining company that produces, processes and sells metallurgical and thermal coal in Virginia and West Virginia. As of December 31, 2021, it operated 20 active mines and 8 coal preparation and load-out facilities.

In the last quarter, Alpha Metallurgical beat earnings estimates by 11% on revenue that beat by 21%. The lone analyst providing estimates on this company seems extremely optimistic. So the 2022 estimate has increased $21.36 (44%) in the last 60 days while the 2023 estimate has increased $19.53 (176%). The analyst expects Alpha Metallurgical’s revenue and earnings to grow a respective 52% and 357% this year.

The Zacks Rank #1 stock has a Value Score of B and Growth Score of A.

Taseko Mines Ltd.

TGB

Vancouver, Canada-based Taseko Mines is a mining company that acquires, develops and operates properties for exploration of copper, molybdenum, gold, niobium and silver deposits. It holds a 75% interest in the Gibraltar mine in British Columbia and a 100% interest in the Yellowhead copper project, the Aley niobium project, and the New Prosperity gold and copper project in British Columbia. It also has a 100% interest in the Florence copper project in Arizona.

Taseko met analyst expectations in the last quarter, and the Zacks Consensus Estimates for 2022 and 2023 earnings are up a respective 2 and 3 cents in the last 60 days. Overall, its revenue and earnings growth expectations for this year are 32% and 108%, respectively.

The Zacks Rank #2 (Buy) stock has Value and Growth Scores of A.

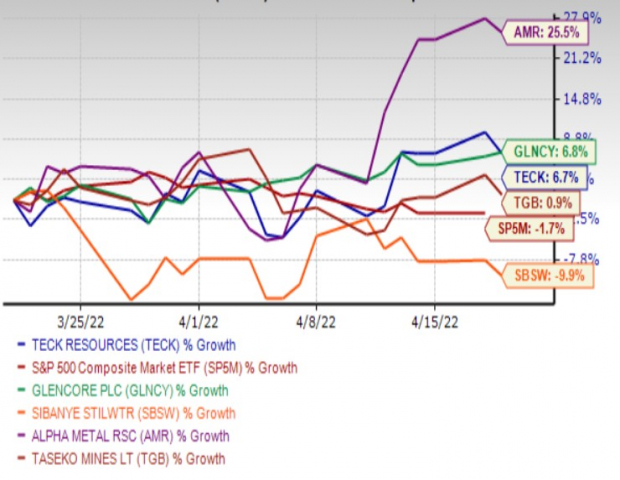

One-Month Price Movement

Image Source: Zacks Investment Research

Zacks Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock and 4 Runners Up >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report