Universal Health Services, Inc.

UHS

recently revised its 2022 outlook due to significant drawbacks in operations witnessed in the first two months of the second quarter. Following the announcement, the stock declined 6.1% yesterday. The effect was witnessed in other hospital operators’ share prices as well.

UHS expects adjusted earnings per share (EPS) for 2022 in the range of $9.60-$10.40, down from the previous estimate of $11.90-$12.90. The revised guidance also indicates a decline from the 2021 figure of $11.82 per share. Adjusted EBITDA is now expected within $1.635-$1.712 billion, down from the previous estimate of $1.830-$1.927 billion.

Net revenues for the year are now expected within $13.235-$13.371 billion, lower than the earlier projection of $13.424-$13.694 billion. However, the guidance is still higher than the 2021 figure of $12.6 billion. For the second quarter of 2022, adjusted EPS is estimated within $2.05-$2.15, indicating a massive decline from the year-ago level of $3.76.

Let’s focus on the causes behind the significant reductions in outlook to get an idea about the common theme witnessed by the hospital operators.

Universal Health’s acute care hospitals experienced lower-than-expected patient volumes in the second quarter, which decreased revenues and profits. While UHS witnessed a substantial decline in COVID-related patients in the quarter, the same was only partially offset by growth in non-COVID patient volumes.

Further, laborshortages and related costs significantly hurt profits. The behavioral health care unit witnessed similar traits of lower patient volumes, revenues and profits. Also, UHS expects a $28-million jump in depreciation and amortization cost for 2022 due to renovations in one acute care facility in California.

The problems stated above are expected to gradually decline in the second half of the year. To counter the situation, UHS is relying on recruitment and retention initiatives, changing patient care models, cost-curbing efforts and contractual negotiations with managed care payers. Moreover, start-up losses incurred from the new facilities are expected to get diluted in the second half.

Other players in the

hospital

space are also expected to opt for aggressive cost-cutting initiatives to boost their profit margins. While the laborshortage continues to be a headwind, the eventual rise in non-COVID patient volumes will likely provide some relief. More contractual negotiations with managed care players are expected to aid the hospital operators.

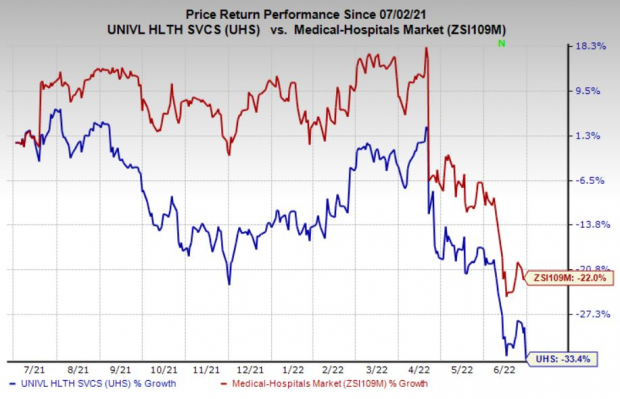

One-Year Price Performance

Shares of Universal Healthhave decreased 33.4% in the past year compared with the 22% fall of the industry it belongs to.

Image Source: Zacks Investment Research

Zacks Rank & Key Picks

Universal Health currently has a Zacks Rank #4 (Sell).

Some better-ranked stocks in the broader

medical

space are

Assertio Holdings, Inc.

ASRT

,

Altimmune, Inc.

ALT

and

UnitedHealth Group Incorporated

UNH

. While Assertio sports a Zacks Rank #1 (Strong Buy), Altimmune and UnitedHealth carry a Zacks Rank #2 (Buy) at present. You can see

the complete list of today’s Zacks #1 Rank stocks here

.

The Zacks Consensus Estimate for Assertio’s second-quarter earnings indicates a 125% improvement from the year-ago quarter’s reported figure. ASRT’s earnings beat estimates twice in the last four quarters and missed the same on the other two occasions, the average surprise being 26.4%.

The Zacks Consensus Estimate for Altimmune’s 2022 bottom line indicates an 8.2% improvement from the 2021 levels. ALT has witnessed four upward estimate revisions in the past 60 days against none in the opposite direction. ALT’s earnings beat estimates in three of the last four quarters and missed the mark once on the remaining occasion.

The Zacks Consensus Estimate for UnitedHealth’s 2022 bottom line indicates 14.4% growth from the year-ago period’s level. UNH has witnessed one upward estimate revision in the past 60 days against none in the opposite direction. UNH’s earnings beat estimates in each of the last four quarters, the average being 3.7%.

Zacks Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock and 4 Runners Up >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report