Myriad Genetics, Inc.

MYGN

has been gaining from strong testing volume growth in the third quarter of 2021. The company’s notable launches of myRisk Hereditary Cancer test as well as the myRisk and RiskScores raise investor confidence. A strong solvency position also buoys optimism. However, escalating expenses and macroeconomic headwinds do not bode well for the stock.

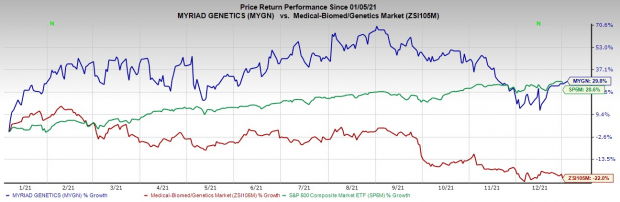

Over the past year, the Zacks Rank #3 (Hold) stock has gained 29.8% against the 22% decline of the

industry

and 28.6% rise of the S&P 500.

The renowned molecular diagnostic company has a market capitalization of $2.34 billion. The company’s earnings surpassed estimates in three of the trailing four quarters and missed in one, delivering an average surprise of 2.9%.

Image Source: Zacks Investment Research

Let’s delve deeper.

Factors At Play

Product Volume Picks Up:

Myriad Genetics continues to record strong testing volumes in third-quarter 2021, raising optimism. Total testing volumes of 252,000 reflected a 15% improvement year over year in the last reported quarter. Meanwhile, GeneSight witnessed robust volume growth within new provider segments, including general practice physicians and nurse practitioners. It is worth noting that digital ordering accounts for 10-15% of all GeneSight orders currently. The prenatal test volumes rose 7% year over year, led by Myriad Genetics’ proprietary AMPLIFY technology.

Product Launches:

We are upbeat about Myriad Genetics’ product launches in recent months. During its third-quarter earnings call, the company noted that following the launch of the myRisk Hereditary Cancer test with a risk score for all ancestries– the first and only test of its kind– it is experiencing growing market interest from unaffected women for hereditary cancer tests. In addition, the GeneSight test, according to Myriad Genetics, is on track to exceed launch objectives in terms of both projected volume and revenues. Earlier, the company announced the launch of myRisk and RiskScores, which marks a significant step toward improving the accessibility to genetic testing.

Strong Solvency:

Myriad Genetics exited the third quarter with cash and cash equivalents of $295.2 million compared with $118.4 million at the end of the last reported quarter. However, the company has no debt on its balance sheet at the end of the third quarter, indicating a strong solvency position.

Downsides

Escalating Expenses:

During the third quarter, Myriad Genetics’ research and development expenses rose 6.8% year over year, whereas selling, general and administrative expenses shot up 45.2% year over year. These escalating operating expenses are building significant pressure on the company’s bottom line.

Foreign Exchange Headwinds:

Myriad Genetics receives a considerable portion of its revenues and pays a portion of its expenses in foreign currencies. As a result, the company remains at risk of exchange rate fluctuations between foreign currencies and the U.S. dollar.

Macroeconomic Woes:

The current macroeconomic situation around the globe is impacting Myriad Genetics’ financials. In its third-quarter earnings update, the company noted that it is experiencing increased inflationary pressure, including higher material costs due to global supply-chain disruptions as well as escalating labor costs.

Estimate Trend

The Zacks Consensus Estimate for Myriad Genetics’ fourth-quarter 2021 earnings is pegged at a penny, suggesting a significant improvement from the year-ago reported loss of 12 cents.

The Zacks Consensus Estimate for its 2021 revenues is pegged at $692.05 million, suggesting an 8.37% rise from the year-ago reported number.

Key Picks

A few better-ranked stocks in the broader medical space that investors can consider are

Apollo Endosurgery, Inc.

APEN

,

Cerner Corporation

CERN

and

West Pharmaceutical Services, Inc.

WST

, each carrying a Zacks Rank #2 (Buy). You can see

the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Apollo Endosurgery has a long-term earnings growth rate of 7%. The company‘s earnings surpassed estimates in the trailing four quarters, delivering a surprise of 25.6%, on average.

Apollo Endosurgery has outperformed its industry in the past year. APEN has gained 135.7% compared with the industry’s 10.5% growth.

Cerner has a long-term earnings growth rate of 13.3%. The company’s earnings surpassed estimates in three of the last four quarters and met estimates in one. Cerner has a trailing four-quarter earnings surprise of 3.2%, on average.

Cerner has outperformed its industry in the past year. CERN has gained 18.7% against the industry’s 39.4% decline.

West Pharmaceutical has a long-term earnings growth rate of 27.6%. The company’s earnings surpassed estimates in the trailing four quarters, delivering an average surprise of 29.4%.

West Pharmaceutical has outperformed its industry in the past year. WST has rallied 53.2% compared with the industry’s 15.4% rise.

Zacks’ Top Picks to Cash in on Artificial Intelligence

This world-changing technology is projected to generate $100s of billions by 2025. From self-driving cars to consumer data analysis, people are relying on machines more than we ever have before. Now is the time to capitalize on the 4th Industrial Revolution. Zacks’ urgent special report reveals 6 AI picks investors need to know about today.

See 6 Artificial Intelligence Stocks With Extreme Upside Potential>>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report